📊 Full opportunity report: The mandate. Why the US conversational- finance surface does not translate to Europe. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

The US launches permissionless financial surfaces, while Europe’s regulatory framework mandates licensing and consent. This fundamental difference alters market dynamics and development approaches.

OpenAI’s personal-finance surface launched in the United States on May 15, 2026, operating permissionlessly through API access without regulatory licenses. In contrast, Europe’s regulatory regime mandates licensing, consent, and compliance for any data access or AI deployment in financial services, preventing a direct US-style launch.

In the US, the surface was built on a permissionless, private infrastructure—Plaid’s API allowed broad, unregulated account access. This enabled rapid deployment and innovation with minimal regulatory hurdles. Conversely, Europe’s open-banking framework, established by PSD2 in 2018 and evolving into PSD3 and FIDA, requires licensed third-party providers to operate under strict regulatory oversight, including consent management and compliance with AI and data regulations.

Furthermore, the EU AI Act classifies certain AI systems used in credit scoring and financial assessment as high-risk, imposing rigorous obligations. This layered, mandate-driven architecture means that any European equivalent of the US surface must be a licensed, consent-based product, not a permissionless API. As a result, European firms are building different products—focused on licensing and compliance—rather than permissionless aggregation. The firms capable of building these are typically incumbents with existing licenses, unlike the US where permissionless innovators thrive.

The mandate.

Why the US conversational-

finance surface does not

translate to Europe.

data, AI — vs zero in the US build

maximum penalty

mandate — is likely operational

bank data · it is a licensed activity

- Access built by private aggregators — Plaid, Yodlee, MX, Finicity

- No banking license required to read bank data

- Read-only design sidesteps money-transmission rules

- No single federal open-banking statute · the surface ships as a product

- Access is a licensed activity — AISP / PISP under PSD2

- Regulator authorization required; no permissionless route

- Explicit, revocable, SCA-governed consent regime

- A directly-applicable rulebook (PSR) · the surface must be licensed

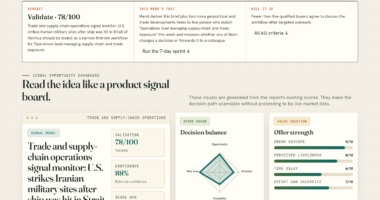

The architecture diverges at the foundation: the American surface treats account access as a product you buy and consent as a button you tap, while Europe treats both as mandates you are licensed and supervised to fulfill. In the US, you ship a finance surface. In Europe, you license one.Thorsten Meyer · The Mandate · Agentic Commerce 03

Implications of Regulatory Architecture on Market Access

This structural difference impacts market entry, product design, and competitive advantage. In Europe, compliance requirements elevate costs, favor established licensed firms, and slow innovation. The architecture shifts the focus from permissionless aggregation to licensed, consent-based services, potentially leading to more secure but less agile consumer financial products. Understanding this difference is crucial for firms aiming to operate across both regions and for policymakers assessing innovation versus consumer protection.

API FIN & BODY CURE Freshwater Fish Powder Medication 10-Count Box

- Package Quantity: 10-Count Box

- Treatment Uses: Treats slime, sores, rot, gill disease

- Water Discoloration: Causes slight water discoloration

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Legal and Regulatory Foundations of US and European Finance Surfaces

The US’s permissionless approach stems from a private, market-driven infrastructure—Plaid and similar firms—allowing rapid deployment without regulatory licenses. The European framework, rooted in PSD2 (2018), evolved into PSD3 and FIDA, establishing a mandated, regulated environment for data access and financial services. The EU’s AI Act, effective August 2026, further classifies high-risk AI, adding layers of supervision by financial regulators like BaFin. These layered regulations create a fundamentally different architecture for financial data and AI use, preventing straightforward US-style launches in Europe.

“The American surface is permissionless; Europe’s is mandate-driven. This difference in architecture determines who can build, how quickly, and at what cost.”

— Thorsten Meyer

Unclear Impact on Consumer Outcomes and Innovation Pace

It remains uncertain whether Europe’s mandated, licensed approach will lead to better consumer protection and security, or if it will slow innovation and concentrate market power among incumbents. The long-term effects of this architecture on competition, product diversity, and consumer choice are still being evaluated.

Next Steps for Market Development and Regulatory Evolution

Regulators are expected to finalize PSD3 and FIDA regulations by 2026-2027, clarifying licensing requirements and data access rules. Firms are beginning to adapt their strategies to the mandated environment, focusing on licensing and consent management. Monitoring how these changes influence innovation, competition, and consumer outcomes will be crucial in the coming years.

Key Questions

Why can’t European firms simply replicate the US permissionless finance surface?

Because European law mandates licensing, consent, and compliance for data access and AI use, preventing permissionless API-based models. European firms must operate within a regulated, licensed framework.

Will the European approach slow down financial innovation?

It is possible. The regulatory requirements increase costs and complexity, which may reduce the speed of innovation but potentially enhance security and consumer protection.

Who is most likely to succeed in building Europe’s finance surface?

Incumbent financial institutions with existing licenses and experience navigating regulation are better positioned to develop compliant, licensed products than permissionless aggregators.

How does the AI Act influence financial AI systems in Europe?

The AI Act classifies certain financial AI systems as high-risk, imposing strict obligations and supervision by financial regulators, influencing how AI is developed and deployed in the region.

What are the main differences between US and European data access models?

The US model is permissionless, relying on private APIs without regulatory licenses, while Europe’s model is mandate-based, requiring licensed providers and explicit consent for data access.

Source: ThorstenMeyerAI.com